If you’ve been investing in cryptos, you may have likely heard the term “wrapped” Bitcoin or wrapped tokens. This article will explore the types of wrapped tokens in the crypto space, why they exist, and what benefit they have to you as a crypto trader or long-term investor.

Blockchains Are Separated

Different blockchains like Ethereum and Bitcoin use different protocols and have different functionalities. Moreover, due to the fundamental differences in their algorithms, they cannot talk to each other. While this independence preserves the blockchain’s sovereignty and increases security, it makes the existence of an interoperable distributed ecosystem with easy data exchange challenging.

The ideals of decentralized finance, or DeFi, is a smooth, efficient, and speedy movement of the value, and this is why wrapped tokens can find a place as a practical application. Newer blockchains, such as Polkadot, were developed to solve the interoperability issue that plagues separate blockchains. However, the need for communication between blockchains became apparent, and this communication was possible through the development of wrapped tokens.

Wrapped Cryptocurrency Basics

Wrapped cryptocurrencies and crypto tokens are cryptocurrencies and assets pegged to the value of another cryptocurrency or asset, such as a precious metal, stock, or real estate, and then minted on a DeFi platform. They have become popular as retail crypto brokers made this asset class more accessible and more advanced in tandem.

The original asset gets “wrapped” into a digital vault, with a newly minted token created, which can be used to transact on another blockchain. These wrapped tokens allow non-native assets to be used on any blockchain, building bridges between different networks and creating interoperability in the crypto space.

Wrapped tokens can be created from any asset, art, commodities, collectibles, equities, real estate, and even fiat currencies. However, because wrapped tokens get “pegged” to another asset, it’s required for them to be managed by a custodial entity that wraps and unwraps the asset. We will be discussing why this is a limitation in the crypto world.

The First Wrapped Cryptos

Bitcoin was the first crypto to be wrapped, and the space is dominated by wBTC, which took bitcoin and put it on the Ethereum blockchain using smart contracts. This allowed investors to earn a passive fixed income. There are now many wrapped tokens, most of which use Ethereum’s ERC-20 format or the Binance Smart chain BEP-20 format.

Interestingly, though ERC-20 tokens are issued on Ethereum, the native ETH token is not compliant with ERC-20 standards because ETH was developed before ERC-20. Therefore, Ether must be wrapped to comply with other ERC-20 token standards. A tokenized wrapped Ether has therefore been created on the Ethereum platform.

Cardano, Solana, and Polkadot have begun experimenting with wrapped tokens, facilitating their access to DeFi applications. More recently, projects included the bETH, a wrapped ETH token, which can be traded freely or used as collateral on protocols of the Ethereum network.

Wrapped Token Types

Stablecoins were, in fact, the first wrapped “tokens.” As a result, they have a significant difference from the more established wrapped “coins.” A stablecoin such as the USDT, the Tether, is, for example, backed by a value of approximately one dollar.

However, Tether does not keep the exact amount of USD fiat currency for each USDT minted; its reserves include other assets besides cash, including cash equivalents, T-bills, and more.

There are two general wrapped token types:

Cash Settled

It is impossible to settle these for their underlying asset, only for their cash value.

Redeemable

These wrapped tokens can be exchanged for their underlying asset.

Non-native blockchains will host these two types of wrapped tokens.

Inner-Workings of Wrapped Tokens

Merchants such as Airswap, AAVE, Ox, Maker, and CoinList will mint the number of original tokens sent on platforms such as Ethereum and act as custodians of that value.

A similar process is used when the wrapped token must be converted back into its original coins, such as Bitcoin, Ether, or the asset. The holder of the wrapped token will request the custodian to release the token from the reserves. For every wrapped BTC, there is a Bitcoin that a custodian is holding.

The process employed for minting and managing wrapped tokens remains a limitation in crypto, as a trusted custodian who holds the funds is required. Unfortunately, this requirement needs to be revised for a decentralized distributed network that is supposed to be trustless.

A custodian is required because traders cannot independently use their wrapped tokens for cross-chain transactions. The technology is, however, evolving, and the potential for decentralized options that solve this problem are appearing.

Wrapped Bitcoin (wBTC)

“Wrapped Bitcoin” was first launched in January 2019 and was the first wrapped Bitcoin. The protocol was designed to bring the potential and liquidity of Bitcoin to the Ethereum network and, in doing so, an ERC-20’s flexibility.

The native BTC was unsuitable for decentralized finance (DeFi) transactions; the wrapped version could be used in place of the original asset to transact within the growing DeFi ecosystem and other Dapps within Ethereum’s network.

The wrapped Bitcoin is a significant addition to the cryptocurrency space. While a wBTC’s value is equivalent to the original Bitcoin, the added functionality accrued with the change to wBTC increases its value allowing it to be used in DeFi applications.

A holder of BTC can lend their Bitcoin via smart contracts by simply connecting their crypto wallet to a decentralized lending platform and earning a fixed interest rate each year. Concurrently, borrowers can use their crypto (BTC) as collateral which could automatically go to the lender in case of a default.

Using this type of financing, holders of the currency can still see returns on their holdings even in bear markets if the value of their asset drops.

Wrapped BTC, Unwrapped

There are three primary actors in wBTC’s creation and management.

The DAO

wBTC’s Decentralized Autonomous Organization comprises 17 members, all from the DeFi space, who hold a multi-signature contract allowing them to add to or remove from the list of wBTC merchants and custodians.

Merchants

These administrators trigger the minting of wBTC by sending a defined amount of BTC to the custodian and requesting the mining of an equivalent amount of the wrapped tokens, defined by the investor’s and trader’s demands.

Custodians

These trusted agents act as vaults who provide reliability and security for wBTC, ensuring that all the wBTC will be backed and verified via an on-chain proof of reserves. Custodians mint the wBTC and send that equivalent amount of wBTC (a one-to-one pegged value of BTC) back to the requesting merchant.

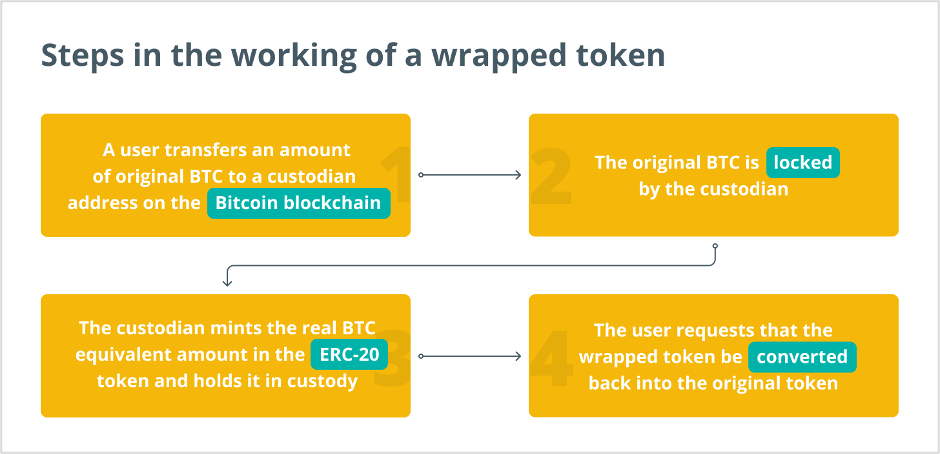

In essence, the merchant transfers the real BTC to the custodian’s address on the Bitcoin blockchain, which is then locked. Once the real BTC is received, the custodian’s address mints the equivalent amount of wBTC on the Ethereum network.

The reverse will happen, and the wBTC will be converted back into real BTC through the burning (destroying) of the ERC-20 BTC token, at which point the locked BTC will be released. The minting and burning of wBTC tokens are tracked and verified on the Ethereum blockchain.

Why Is There wBTC?

wBTC was created because of the growth of DeFi applications which are now valued in the billions of dollars. These tokens are sent to lending platforms, options, derivatives, and other financial applications.

The demand for BTC use as an underlying asset in DeFi was such that it needed to be converted to ERC-20 compatible tokens to participate in Ethereum ecosystem Dapps.

Are They Safe?

From a technical viewpoint, a wrapped Bitcoin token is safe. The original BTC will be in the custody of safe platforms like Ethereum or the Binance Smart Chain. When it is converted to an ERC-20 or BEP-20 token, it will maintain the security of the interconnected network.

A flaw with the wrapped BTC tokens is the need for trust in a custodian that holds the underlying asset. If that custodian unlocks and releases the Bitcoin to someone else, the ERC-20-compatible wrapped Bitcoin holders would be holding a worthless asset.

How the original Bitcoin is held determines the security level provided.

Centralized Custodial Bridge

For example, this organization promises to mint the ERC-20 tokens. The centralized entity must be trusted to hold BTC and not abscond. Users must ensure that these organizations are backed with guarantees and insurance in case something terrible happens.

Decentralized smart contract bridge

These would be the best choice in the crypto world. There would be no need to trust a third party, only the immutable time-stamped intelligent contract coding.

The security of wrapped BTC bridges, crossing different chains, has resulted in several arguments in the DeFi community because of the need to rely on custodians to keep the real BTC locked and their financial incentive not to.

Closing Thoughts

Arcane Research reports that the amount of Bitcoin currently locked on the Ethereum blockchain has grown to $3.5 billion as of Dec 2022 (similar to the 3.6 billion Coinbase estimate above). In addition, it is estimated that over 1% (215,800) of Bitcoin’s current supply of 19.2 million coins is now being used in DeFi, all through wrapped tokens of various types.

Wrapped tokens increase the liquidity and capital efficiency of centralized and decentralized exchanges due to their capability to move assets across multiple blockchain platforms that otherwise would have remained isolated.

Additional advantages wrapped tokens provide speedy transaction times and lowered fees possible with newer blockchains, exceeding the capabilities of older blockchains like Bitcoin and Ethereum’s first generation.

Wrapped tokens also offer fractionalized ownership which is not usually possible for some underlying assets such as art, collectibles, or a classic car. We might see wrapped tokens appearing with discount trading platforms or as part of greater liquid portfolios.

These asset-packing solutions make bitcoin and, more importantly, other assets more useful. We will see many items wrapped into fungible and nonfungible tokens that can be used in the DeFi and metaverse moving forward. The ERC-20 and BEP-20 token formats make the world of DeFi possible.

Disclaimer: The information provided in this article is solely the author’s opinion and not investment advice – it is provided for educational purposes only. By using this, you agree that the information does not constitute any investment or financial instructions. Do conduct your own research and reach out to financial advisors before making any investment decisions.

The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, www.deltecbank.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, www.deltecbank.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}