The impact of artificial intelligence (AI) in the insurance industry has been significant in the past five years. According to Accenture, the adoption of AI in the insurance sector is expected to double in the next three years. It could lead to cost savings of up to $1.2 billion annually.

Another study by PwC found that 63% of insurance companies have already implemented or are planning to implement AI in their business operations. As a result, AI has allowed insurance companies to improve customer experience, reduce costs, and streamline underwriting processes, leading to a more efficient and profitable industry.

What Is AI in Insurance?

Artificial intelligence (AI) in insurance refers to using advanced technology, such as machine learning, natural language processing, and computer vision, to automate and optimise various functions in the insurance industry.

This includes underwriting, claims processing, fraud detection, and customer service. By leveraging AI, insurance companies can analyse vast amounts of data, make predictions, and provide personalised services to customers in real-time. The integration of AI has the potential to transform the insurance industry by improving efficiency, reducing costs, and enhancing the customer experience.

Why Does Insurance Need AI?

There are several reasons why the insurance industry needs AI in 2023 and beyond:

- Increased efficiency and cost savings: AI can automate manual processes and help insurers analyse large amounts of data quickly and accurately, leading to faster decision-making and cost savings.

- Improved customer experience: AI can provide personalised recommendations and real-time support to customers, helping insurance companies meet their evolving needs and preferences.

- Enhanced risk assessment: AI can analyse historical data and other relevant information to identify and assess risk factors, helping insurers make more informed decisions.

- Fraud detection: AI can help insurers detect fraudulent activities by analysing patterns and anomalies in data, reducing the risk of financial losses.

- Better decision-making: AI can provide actionable insights to insurance companies, helping them make more informed decisions and improve their operations.

Given AI’s numerous benefits, it is likely that the insurance industry will continue to adopt and integrate this technology in the coming years. This article will examine some of these areas in more detail.

The Challenge for Legacy Insurers

Legacy insurers must invest in AI to keep up with fintech start-ups because these start-ups often have a technology-first approach and can offer innovative, personalised services to customers in real time. AI can help legacy insurers automate manual processes, provide better customer experiences, and make more informed decisions, allowing them to compete with fintech start-ups and remain relevant in the market.

An example of a legacy insurer investing in AI is AXA, one of the world’s leading insurance companies. AXA has integrated AI into its operations, using machine learning to automate manual processes, improve risk assessment, and provide personalised recommendations to customers.

Another example is Allianz, which has invested in AI to enhance its underwriting processes and improve its efficiency. These companies recognise the importance of AI in staying competitive and relevant in the market and are taking steps to integrate this technology into their operations.

The Rise of Gen Z

Insurance companies need to invest in AI to keep up with the demands of Gen Z tech-savvy buyers who demand fast, convenient, and personalised experiences. AI can help insurance companies automate manual processes, provide real-time support, and deliver personalised recommendations, meeting the demands of this demographic.

Insurance companies use AI to analyse social media data and understand customer preferences and behaviours to meet Gen Z’s demands. For example, an insurance company might use AI to analyse customer interactions on social media platforms, such as Facebook or Instagram, to determine which products and services are most relevant to them.

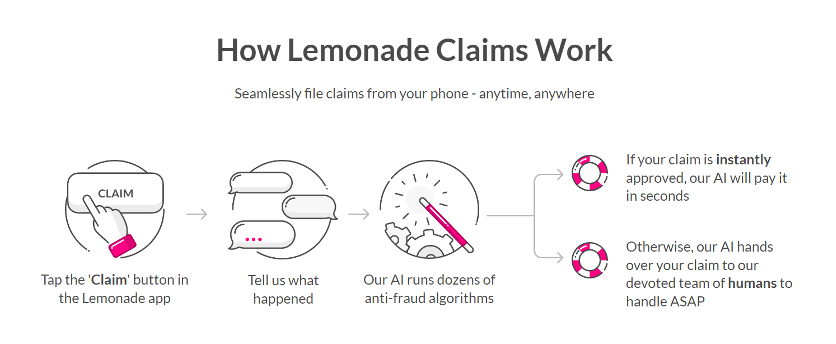

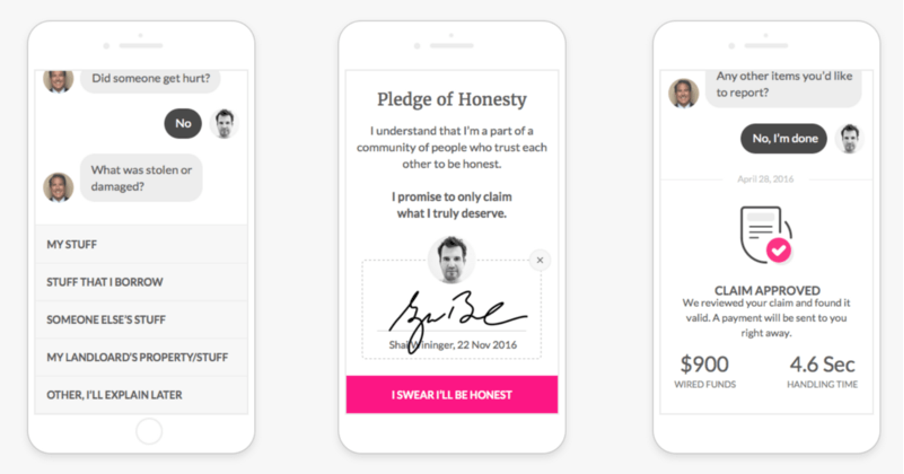

One insurance company that is already using social media to its advantage for Gen Z is Lemonade. The company has built a chatbot that uses natural language processing to handle customer inquiries and uses AI algorithms to process claims quickly.

Using AI to understand customer behaviour and preferences, Lemonade can provide a personalised experience that appeals to Gen Z buyers. This demonstrates how insurance companies can use AI to keep up with the demands of this demographic and remain competitive in a rapidly evolving market.

AI for Efficiency and Cost Savings

Insurance companies use AI to improve efficiency and reduce costs by automating manual processes and making more informed decisions. AI algorithms can quickly analyse large amounts of data, identify patterns, and make predictions, allowing insurance companies to make more informed decisions and reduce the time and resources required to complete tasks.

For example, some insurance companies use AI to automate the underwriting process, reducing the time and resources required to assess risk and provide quotes. Others use AI to automate claims processing, reducing the time required to process claims and improving the overall customer experience.

MetLife is one insurance company already utilising AI to increase efficiency and save costs. AI has been incorporated into the company’s operations, with algorithms used to automate procedures, enhance risk assessment, and deliver tailored suggestions to consumers. Using AI, MetLife can improve customer service, save operating expenses, and increase operational efficiency.

Improving Customer Service

Insurance companies use AI to improve the customer experience by providing more personalised services and real-time support. For example, AI algorithms can analyse customer data and preferences to provide tailored recommendations, and chatbots powered by natural language processing can provide instant customer support. These technologies allow insurance companies to provide a faster, more convenient, and more personalised experience, meeting the demands of modern customers.

One insurance company already using AI to improve customer experience is Oscar Health. The company uses AI to personalise the customer experience, from identifying and addressing potential health issues to providing care recommendations. Oscar Health uses machine learning algorithms to analyse customer data, such as claims and health records, to identify potential health issues and provide personalised recommendations to customers.

By using AI to provide a more personalised experience, Oscar Health can meet its customers’ demands and provide a level of service that sets it apart from other insurance providers. This demonstrates how insurance companies can use AI to improve the customer experience and remain competitive in a rapidly evolving market.

Enhancing Risk Assessments

Insurance companies use AI to enhance risk assessment by providing more accurate and reliable data analysis. AI algorithms can quickly analyse large amounts of data, identify patterns, and make predictions, allowing insurance companies to make more informed decisions and better assess risk. This helps insurance companies reduce fraud risk and underwrite policies more effectively, improving the overall customer experience.

One insurance company already using AI to enhance risk assessment is Allstate. The company uses AI algorithms to analyse customer data, such as driving patterns and vehicle usage, to assess risk and provide personalised insurance coverage. Allstate’s AI system can quickly process large amounts of data and identify patterns that might indicate increased risk, allowing the company to make more informed decisions and better assess risk.

Using AI to enhance risk assessment, Allstate can provide better customer service and remain competitive in a rapidly evolving market. This demonstrates how insurance companies can use AI to drive operational efficiency, reduce costs, and improve customer experience.

Using AI to Detect Fraud

Insurance companies use AI to detect fraud by analysing large amounts of data to identify suspicious patterns and anomalies. AI algorithms can quickly process data, identify red flags, and trigger investigations, helping insurance companies prevent fraud more effectively.

One insurance company that is using AI to detect fraud is Anthem. The company uses AI algorithms to analyse customer data, such as claims and payment history, to identify suspicious patterns and trigger investigations. Anthem’s AI system can quickly process large amounts of data and identify red flags, such as unusual billing patterns or repeated claims from the same provider, allowing the company to detect fraud more effectively.

Using AI to detect fraud, Anthem can reduce the risk of financial losses and improve the overall customer experience. This demonstrates how insurance companies can use AI to enhance security, reduce costs, and remain competitive.

Creating Actionable Insights

Insurance companies use AI to create actionable insights by analysing large amounts of data to identify patterns, make predictions, and inform business decisions. AI algorithms can quickly process data, identify trends, and provide real-time insights, allowing insurance companies to make data-driven decisions and improve the overall customer experience.

Some examples of insurance companies using AI to create actionable insights include Allstate, Metromile, and Lemonade.

Allstate uses AI to assess risk and provide personalised insurance coverage by analysing customer data, such as driving patterns and vehicle usage. Metromile uses AI to analyse telematics data from connected vehicles to provide real-time insights and inform pricing and underwriting decisions. Finally, lemonade uses AI to automate the insurance process, making it faster and more efficient to create actionable insights that drive business decisions and improve the overall customer experience.

Closing Thoughts

AI is having a significant impact on the insurance industry, transforming the way that insurance companies operate and interact with customers. AI is helping insurance companies to improve efficiency, reduce costs, enhance risk assessment, detect fraud, and create actionable insights.

In the next ten years, the use of AI will likely continue to grow, leading to more advanced and sophisticated applications of AI in areas such as underwriting, claims to process, and customer service.

As AI becomes more prevalent in the insurance industry, we will likely see a shift towards more data-driven, personalised, and automated insurance services that deliver improved customer outcomes and increased efficiency for insurers. With the continued growth of AI in insurance, the industry will continue to evolve and adapt to meet the changing needs of customers and remain competitive in a rapidly changing market.

Disclaimer: The information provided in this article is solely the author’s opinion and not investment advice – it is provided for educational purposes only. By using this, you agree that the information does not constitute any investment or financial instructions. Do conduct your own research and reach out to financial advisors before making any investment decisions.

The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, www.deltec.io.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, www.deltec.io.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.

{kind=link}