Like NFTs, one of the new hot topics in the DeFi space is synthetic crypto assets or tokens. We will introduce these new players in a quick and efficient way, explaining why there is so much buzz behind them, and tell you the important things you need to know about this promising digital asset sector.

DeFi Is Here

Decentralized finance (DeFi) is turning the financial and monetary worlds on their heads. While many DeFi products and services appear familiar, such as exchanges, borrowing, lending, and swaps, blockchain tech’s transparent and open nature means that we can move into a completely novel terrain.

When we look at the lending space, we are able to see how DeFi is bringing a financial paradigm switch in the form of synthetic assets. These novel creations, which are sometimes referred to as “synths,” are blockchain-based cryptocurrency derivatives. Synths act and feel like traditional derivatives but are not at all ordinary.

What Are DeFi’s Synthetic Crypto Assets?

Even with their futuristic-sounding name, synthetic assets are not a difficult concept to understand. At their core, synthetic assets are just derivatives set up on a blockchain.

Imagine that a particular derivative’s value is tied to another asset’s value via a contract. In this case, we can trade the movement of the derivative’s value using financial products such as futures or perpetuals.

How do synths differ from traditional derivatives like futures?

Synths are possible because of smart contract technologies. Rather than using contracts to create the chain that binds an underlying asset with the derivative product, synthetic assets will tokenize the relationship. Tokenization means that the synthetic asset can impart exposure to any asset no matter what it is and no matter where it is, all from within the crypto ecosystem via a smart contract.

In short, a synthetic asset is just a tokenized derivative that mimics the value of another asset. Smart contract tech allows developers to create these synthetic assets and then trade them on blockchains. Synthetic stocks represent shares that generally trade on the Nasdaq or NYSE, but synths can trade on a blockchain-based exchange.

Imagine you want to trade in Saudi Aramco stock which is only on the Saudi stock market and has restrictions for foreign ownership. Only the most significant foreign investors may buy Saudi stocks directly, so non-billionaires can only find exchange-traded funds (ETFs) focused on Mideast investments.

Using a synth, you could trade $sSAR (synthetic SAR) instead, which behaves like its underlying asset, tracking its price with data oracles like Chainlink. Oracles are entities connecting blockchains to external systems, providing accurate data, thereby enabling smart contracts to operate efficiently.

Synthetic’s Advantages

Derivatives were a groundbreaking change to finance, with their ability to unlock additional value through volatility. However, blockchain-based synthetics could take liquidity access to a new level.

Here are the primary advantages that synthetic assets can provide to the markets beyond traditional derivatives.

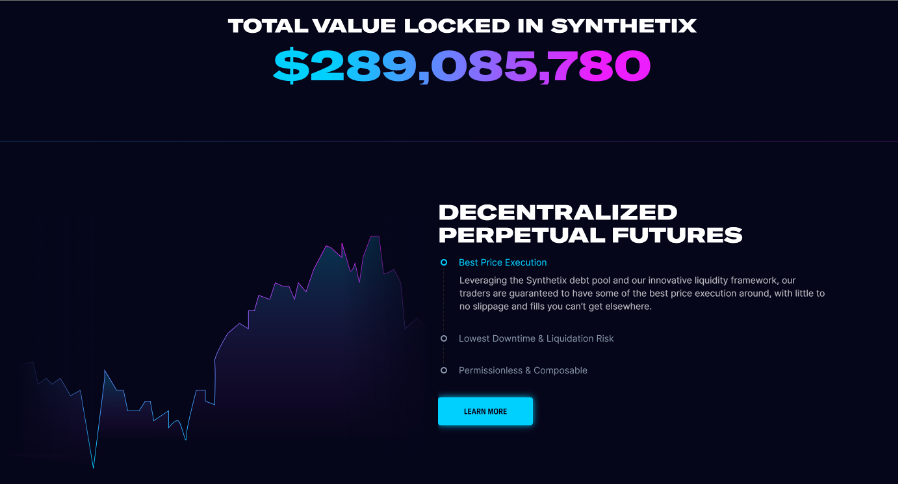

Issuable by anyone. Crypto-based synthetic assets can be minted by anyone through open-source protocols like Synthetix or Mirror. Synthetix already has over $289 million in assets locked in its protocol.

Global liquidity. Synths could be traded on any crypto exchange, including the unregulated, decentralized exchanges.

Borderless transfers. Synthetic crypto assets are similar to ERC-20 tokens on the blockchain, and you can send or receive them with standard cryptocurrency wallets.

Frictionless exchange. Owners are able to switch between synthetic equities, synth metals, and other digital assets like NFTs without having to hold the underlying asset.

Liquidity pool farming. Synth securities can participate in yield farming, or the ability to generate a yield on a synth position by contributing a quantity of the native crypto to liquidity pools. A liquidity pool is a quantity of cryptocurrency locked in a smart contract.

In general, synthetic assets allow for much more liquidity between global exchanges, swapping between protocols via bridges.

The Tokenization of Anything

The closer we look at synthetic crypto assets, the more pronounced their power becomes. They can be utilized to represent anything, not just traditional equity assets.

Any asset can be represented as a synthetic asset token and then be brought to the blockchain space. This ability to tokenize anything means that synthetic assets can unlock an infinite number of pools for global liquidity. Beyond the simple trading of synthetic assets, synths can create possibilities for a wealth of new markets.

A Novel Synth

A synthetic asset token can be created to track the corporate CO2 emissions found in an industrial zone. When the emissions rise, the token holders (city officials, outside speculators, locals living close by) will profit as the offending companies issue CO2 tokens.

However, if the emissions decrease, then the companies will benefit by retaining their tokens. In the long run, this incentivizes companies to continually reduce their CO2 emissions. This is just a simple example of how synthetic asset-based markets that are not currently in place can expand the opportunities for new types of value creation.

Understanding the Mirror and Synthetix Protocols

Synthetic crypto assets are already trading in ways most would find familiar, making these new assets more approachable to anyone with experience trading equities or cryptos.

Synthetix.io. This is the most well-known decentralized synthetic asset exchange protocol. Users can mint, exchange, and provide liquidity to a vast array of new assets.

Mirror.finance. Despite its start by a centralized company, Mirror is a decentralized synthetic asset protocol capable of creating and exchanging fungible tokens that follow and cross chain assets’ prices.

Users of Mirror and Synthetix trade stocks like Amazon, Apple, Tesla, and Twitter as easily as they could on any centralized trading platform, such as WeBull or Robinhood. But users can do much more than what is possible with those platforms.

Oracles provide real-time data. The target asset price is provided by an oracle enabling the synthetic asset to track the underlying asset’s value accurately.

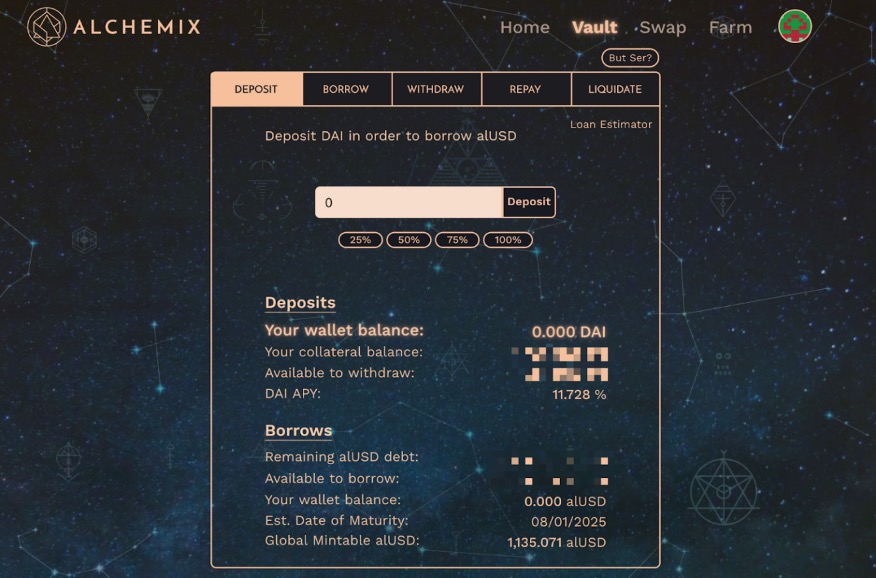

Users mint (create) new assets. They will deposit collateral in the form of SNX for Synthetix and UST for Mirror. This collateral is used to back the newly minted asset with a tangible value.

Users trade synthetic assets. Traders can utilize the liquidity pools of Synthetix or Mirror to trade synthetic asset derivatives such as mETH (mirrored Ethereum), sUSD (synthetic USD), or popular equities like mGME (mirrored Gamestop). These are trading pools that are always open. There is no blocking of stock purchases or short sales, like what happened with Robinhood and Gamestop.

Minters gain liquidity creation rewards. These are provided through the exchange-traded assets that a minter creates. Meaning, they are paid in the native asset for the protocol (i.e., MIR or SNX).

New Synthetic Asset Exchanges

The synthetic trading space is expanding quickly, though Mirror and Synthetix are the oldest and the market leaders. There are several up-and-coming exchanges throwing their hats into the ring.

UMA is creating synthetic assets for Web 3.0. It calls itself an “optimistic oracle and dispute arbitration system” intended to securely bring arbitrary types of data on-chain.

Linear Finance calls their synths “liquid assets,” having the same value as other assets simulating commodities, cryptos, and other digitally structured products.

Balanced DAO is the finance system found on the ICON network backed with ICX tokens.

Deus.Finance is the marketplace of decentralized financial services providing synth trading infrastructure on Ethereum. They have also created a “Version 2” that includes minting DEI, or a cross-chain stablecoin.

Closing Thoughts

When looking at the world of finance, cryptos comprise only a tiny portion. Synthetics are able to tap into the broader market and provide services that the traditional stock exchanges cannot. These assets are growing in popularity, and in the United States, they remain highly regulated.

This growth is being led by “Synth Funds” that follow ETFs, such as an S&P 500-following ETF. The possibility of additional liquidity and borderless transferring makes these new products highly sought after. They have the potential to permanently change the financial trading landscape.

Disclaimer: The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, www.deltecbank.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, www.deltecbank.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees. This information should not be interpreted as an endorsement of cryptocurrency or any specific provider, service, or offering. It is not a recommendation to trade.