Uber and Lyft have changed the short-distance ride-hailing market once belonging to the local and usual handful of taxi companies. As they took over these new markets, they also changed the way we thought about travel.

Further, asking friends for a ride to the airport is beginning to disappear with the onset of autonomous vehicles. Several new companies are testing this out, and some are in full operation in limited areas with complete, autonomous ride-share services. We take a deep dive into the current state of the autonomous ride-hailing market.

The Rise of Autonomous Vehicles

Autonomous technology is the next stage for the travel industry. The growing success of the electric vehicle set the tone, even if battery costs have a long way down to go. But it’s better to call this one door leading to many.

For example, artificial intelligence will play a crucial role in the use of autonomous ride-hailing. We have: route optimization, accident prevention, and maximized utilization (keeping all vehicles active). Not only does this lower costs for companies entering this space, it dramatically improves urban efficiency.

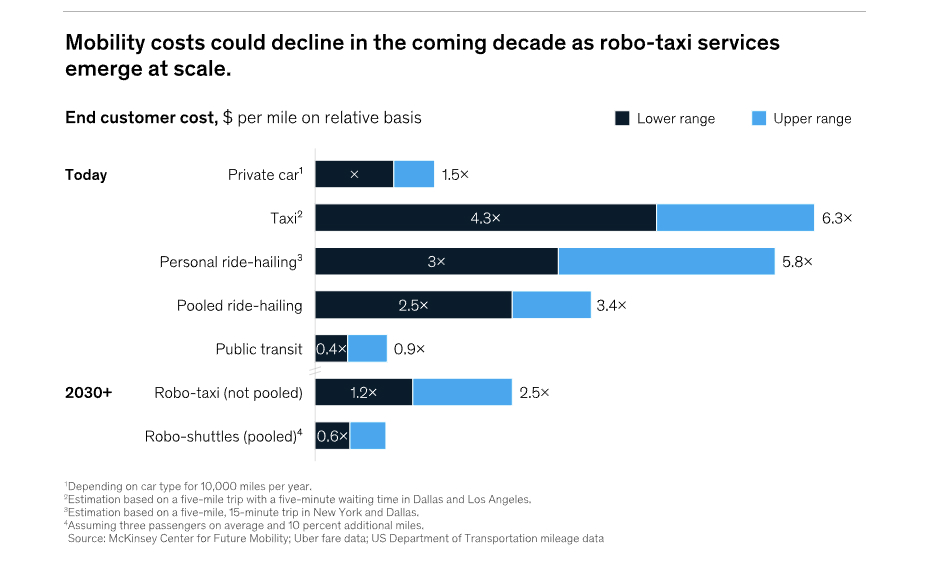

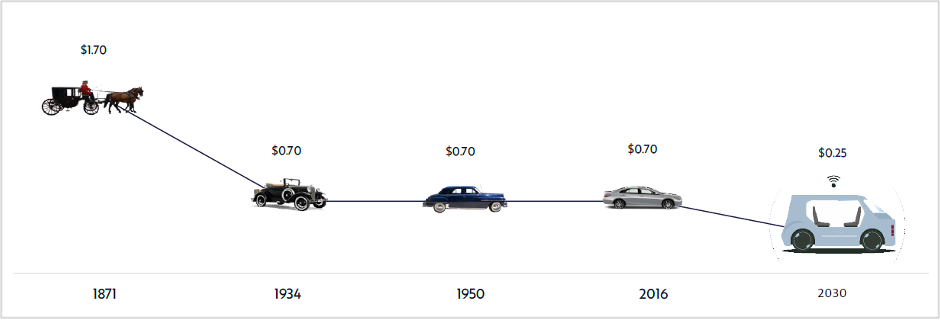

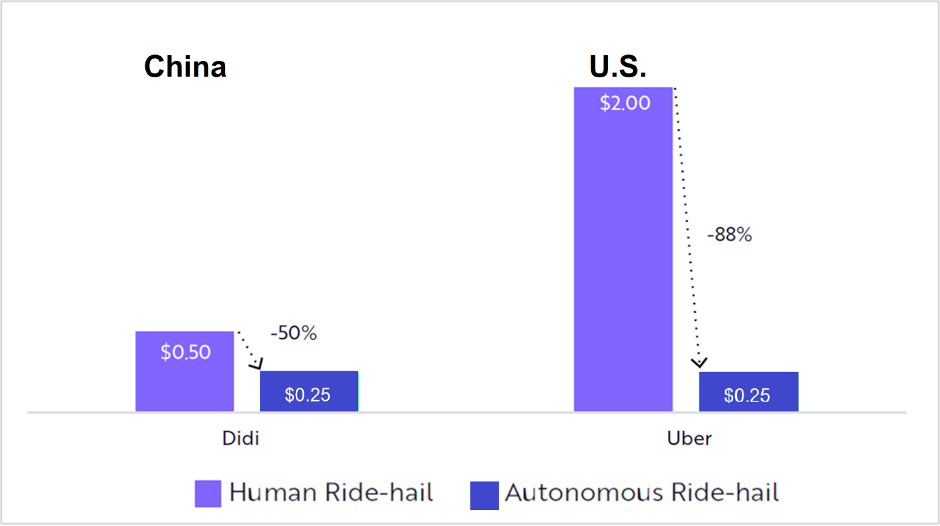

ARK Investment Research has predicted that the price of autonomous electric vehicle transportation will fall to $0.25 per mile by 2030.

These three factors will drive the cost of ride-hailing services. However, industrialized countries will also see a massive reduction in the cost per mile as labor makes up over 70% of the cost, which is followed by the vehicle itself, and its fuel and maintenance. ARK Research has estimated that the price per mile could be reduced by up to 88% for an autonomous ride-hail.

The autonomous ride-share total addressable market (TAM) is estimated to reach between $11 and $12 trillion for two key reasons.

1. High utilization rates. Electric autonomous vehicles can provide rides to clients 24 hours a day, only offline during charging and maintenance times.

2. Low operation costs. The cost of a ride-hail will drop to $0.25 due to several factors. Accidents per mile driven by autonomous vehicles are already lower than by human drivers, and with more autonomous vehicles on the roads, this will drop further. Autonomous vehicles drive in a more efficient way, also reducing fuel costs up to 44% for passenger vehicles and 18% for trucks.

Autonomous Ride-Share Programs

Cruise

Cruise is a subsidiary of General Motors and became the first company to begin an autonomous ride-hailing service in a major city. In June 2022, Cruise received approval from the California Public Utilities Commission and started its public, driverless, fared, autonomous ride-hailing.

Cruise launched with a fleet of 30 autonomous all-electric Chevy Bolts. These small cars ferry passengers around many parts of the city, and the service is currently available daily from 10 p.m. to 6 a.m. (provided “normal” weather conditions).

Cruise vehicles are limited to a maximum of 30 mph and cannot operate if there is heavy rain, fog, smoke, hail, sleet, or snow. Cruise is looking to add more Chevrolet Bolts to its fleet and increase the time it’s allowed to operate.

Since 2020 Cruise has delivered a total of 2.2 million meals to San Francisco’s needy through a partnership with local food banks. Cruise has also begun the groundwork for autonomous ride-hailing services to launch in Dubai in 2023 and later in Japan.

Baidu

Chinese Technology giant Baidu began its Autonomous Driving Unit (ADU) in 2014 to design vehicles that could move passengers without the need for a driver. Baidu launched its “Apollo Go” self-driving robo-taxi business in 2017, and they recently upped the ante with their Baidu Apollo RT6 Autonomous Driving Vehicle in July 2022.

In that same month, they received approval from the Beijing authorities to launch a robo-taxi service within a Beijing suburb. The new Apollo RT6 has a detachable steering wheel because the car no longer needs a driver.

In August 2022, Baidu also obtained the permits to operate a fully autonomous taxi service in two Chinese megacities, Wuhan (11 million residents) and Chongqing (30 million residents). Baidu’s 100% autonomous robo-taxi services will begin on a small scale with a fleet of only five vehicles in each city and provide their service in designated areas from 9:30 a.m. to 4:30 p.m..

Pony.ai

Pony has also received permits from Beijing authorities to provide their fair-charging, driverless robo-taxi service in July 2022. With this new permit, they are now able to charge fares for rides within a 60 square kilometer area (23.1 sq miles) in Beijing’s Yizhuang suburb.

The service area includes public facilities like underground stations, parks, and sporting centers, as well as key residential and business districts. The new permit builds upon two other recent Beijing autonomous vehicle milestones. Pony.ai was allowed to launch a robo-taxi service with safety drivers in November 2021.

Since November 2021, Pony.ai has provided over 80,000 rides from 200 pickup or drop-off locations. And by July 2022, their robo-taxi service called “PonyPilot+” completed a total of 900,000 orders with nearly 80% from repeat customers. Further, 99% of the passengers provided positive reviews once the trip was complete, with an average 4.9-star rating on a 5-point scale.

Hyundai Motors

Korean automaker Hyundai launched is RoboRIde autonomous ride-hail service in Gangnam Seoul. The South Korean Land, Infrastructure, and Tourism Ministry issued Hyundai with permits to operate their autonomous vehicles in Seoul.

The Seoul Metro Government established a system that connects traffic signals with autonomous vehicles. This system also supports autonomous vehicles with remote functions, such as lane changing under circumstances where fully autonomous driving is not feasible.

Hyundai has been testing autonomous driving in Gangnam since 2019. The program so far includes only two self-driving IONIQ-5 vehicles, operating from Monday to Friday from 10 a.m. to 4 p.m. with up to three passengers. The program is slated to expand to the general public after successful tests.

Waymo One

The autonomous ride-hailing service from Alphabet (Google) started as the Google Car and has been running autonomous rides in the Phoenix metro area. It has recently expanded its program from the east valley suburbs, where it’s charging fares, to a new pilot program in central Phoenix.

Both services run 24 hours a day, seven days a week. In their 2021 safety report, Waymo states that they have driven millions of miles on public roads in their ten years of service and, with simulations, have completed billions of driving miles.

Closing Thoughts

As the number of autonomous vehicle ride-hailing projects increases, we will become increasingly used to the idea. The number of miles driven (both actual and virtual) will continue to grow, and as this happens, the insurance industry will begin to push toward autonomous driving.

For the U.S.A. and other industrialized countries, the driving costs are high for human-driven vehicles. Economics alone will push for autonomy. The benefits of optimized fuel use and reduced traffic will continuously argue in favor of autonomous driving. We will soon all be passengers.

Disclaimer: The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, www.deltecbank.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, www.deltecbank.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.