Blockchain technology has revolutionised how we think about asset ownership, management, and investment. Tokenization is one of the many innovations that have arisen from this technology. It can disrupt existing asset life cycles, accelerate product innovation, and create customised, hyper-personalised options for investors.

This article will explore tokenization and how it differs from traditional methods. We will delve into the benefits and drawbacks of tokenization, examine real-world use cases, and analyse market statistics to gain a deeper understanding of this transformative technology.

What Is Tokenization?

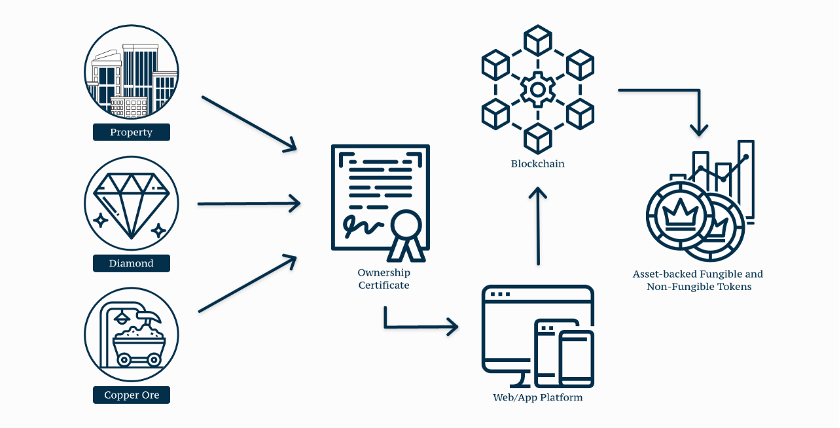

Tokenization is a process that involves converting traditional assets, such as real estate, artwork, or securities, into digital tokens that can be traded on blockchain networks. These tokens are essentially digital representations of the underlying assets.

They provide investors with a way to own and trade assets in smaller fractions rather than owning the entire asset outright. This allows for increased liquidity, lower barriers to entry, and greater transparency. Think of it like a digital representation of a physical asset, which can be bought and sold in smaller parts, with ownership tracked securely and transparently on a blockchain network.

One real-world example of tokenization in finance is the tokenization of company shares. In traditional finance, owning shares in a company means holding a paper certificate or digital record representing a percentage of ownership. This makes it difficult to trade or sell smaller portions of the shares, as the minimum tradable amount is usually one full share.

With tokenization, a company can convert their shares into digital tokens representing smaller ownership fractions. For example, a company could tokenize its shares, with each token representing one thousandth of a share. Investors can then purchase as many tokens as they wish, allowing them to invest in the company with smaller amounts of capital.

Another example is payment card tokenization. Payment card tokenization is replacing sensitive payment card information, such as the card number, with a unique token. This token can then be used in place of the actual card information for payment transactions. Here is a simplified explanation of how payment card tokenization works:

- When a customer provides their payment card information during a transaction, the merchant’s payment processor securely captures the information.

- The payment processor then generates a unique token to represent the card information.

- The token is securely stored in the payment processor’s system, along with reference to the original card information.

- When a payment transaction is initiated using the token, the payment processor retrieves the original card information using the reference and completes the transaction on behalf of the customer.

- The merchant never sees or stores the customer’s payment card information, which helps to protect against data breaches and fraud.

- The token can only be used for transactions with the specific merchant or payment processor that generated it and is useless to anyone who may intercept it.

Overall, payment card tokenization helps to increase the security and privacy of payment transactions by reducing the amount of sensitive information that is shared and stored.

The Technology Behind Tokenization

The technology behind tokenization is based on blockchain, a distributed ledger technology that allows for secure, transparent, and tamper-proof data recording. When an asset is tokenized, it is converted into a digital representation on the blockchain network. This digital representation is called a token, essentially a unique string of code representing ownership of the underlying asset.

Tokens can be programmed to represent various types of assets, such as real estate, artwork, stocks, or commodities. The programming of tokens can be customised to meet the specific needs of the asset being tokenized. For example, a token can be programmed to represent a certain fraction of an asset, or it can be programmed to pay out a certain percentage of returns on the asset.

Tokenization also offers greater transparency and security. Because ownership of tokens is recorded on a blockchain network, it is tamper-proof and transparent. This makes it easier to verify ownership and track the movement of assets, which can help to prevent fraud and other illegal activities.

Financial Use Cases

Tokenization has several use cases in finance that can benefit both issuers and investors. Here are some of the most common use cases for tokenization in finance.

Fractional ownership. Tokenization allows investors to buy and own a fraction of an asset that was previously not possible due to high entry barriers. For example, a piece of real estate can be tokenized and divided into multiple digital tokens, allowing investors to buy and sell a fraction of the property. This opens up new investment opportunities for retail investors and reduces the risk associated with owning a single asset. Companies like Harbor are using tokenization to offer fractional ownership in real estate assets.

Capital raising. Tokenization can be used to raise capital for new projects or businesses. By issuing digital tokens, companies can raise funds from a global pool of investors without the need for intermediaries like investment banks. This can be a more efficient and cost-effective way to raise capital. Companies like Securitize and Tokeny are providing tokenization solutions for capital raising.

Trading and liquidity. Tokenization can make it easier to trade assets that were previously illiquid or traded on traditional markets with high fees and barriers to entry. Digital tokens can be traded 24/7 on decentralised exchanges, increasing liquidity and reducing trading costs. Companies like tZERO and OpenFinance are building decentralised exchanges for tokenized securities.

Compliance and regulation. Tokenization can help issuers comply with securities regulations by automating compliance checks and providing transparency in ownership and transactions. Blockchain networks can also ensure that only authorised investors can trade certain securities. Companies like Polymath and TokenSoft are providing compliance solutions for tokenized securities.

Tokenization has several use cases in finance, including fractional ownership, capital raising, trading and liquidity, and compliance and regulation. Companies like RealT, Securitize, tZERO, and Polymath are using tokenization to disrupt traditional finance and offer new opportunities to investors.

Challenges of Tokenization

While tokenization offers several advantages over traditional finance, several challenges need to be addressed.

Regulation. Tokenization requires compliance with various regulations and laws, which can vary by jurisdiction. This can be challenging for companies that operate across multiple regions and must navigate different regulatory frameworks.

Liquidity. Tokenized assets can be illiquid, meaning they may not be easily tradable or exchangeable. This can be a significant challenge for investors who need to sell their assets quickly or for companies that need to raise capital.

Investor protection. Tokenized assets may not have the same level of investor protection as traditional securities, such as shareholder voting rights or disclosure requirements. This can increase the risk of fraud or abuse.

Interoperability. Tokenization requires interoperability between different platforms and systems, which can be challenging due to the lack of standardisation in the industry.

Adoption. Tokenization is a relatively new concept, and many investors and businesses may be hesitant to adopt it due to the lack of understanding or familiarity with the technology.

Despite the challenges of regulation, tokenization also has the potential to increase compliance and reduce fraud. Tokenized assets can be subject to ‘smart contracts’, which are self-executing agreements that can automate compliance requirements and reduce the risk of fraud or errors in the investment process. This can increase trust in the investment process and reduce the need for costly and time-consuming audits and regulatory oversight.

In terms of liquidity, while tokenized assets may be illiquid in some instances, as we’ve already noted, tokenization can also increase liquidity for assets that were previously illiquid or difficult to trade. Tokenization can enable secondary asset markets, increasing liquidity and providing an exit strategy for investors.

Ultimately, the benefits of tokenization outweigh the potential disadvantages.

Closing Thoughts

Tokenization has the potential to be a genuine disruptor in the finance industry, particularly within asset management. Tokenization enables fractional ownership of assets, opening up investment opportunities to a broader range of investors and increasing liquidity for previously illiquid assets. Additionally, tokenization can increase transparency and efficiency in transactions, reduce fraud and increase compliance while potentially lowering costs.

However, there are challenges to overcome, such as regulatory compliance, interoperability, and investor protection. Adopting tokenization may be slow due to a lack of familiarity with the technology and concerns about the risks and benefits.

Overall, while tokenization has the potential to be a game-changer, its success will depend on overcoming these challenges and convincing investors and businesses of its value proposition. If successful, tokenization could benefit the finance industry significantly, revolutionising the investment process and opening up new opportunities for investors and companies alike.

Disclaimer: The information provided in this article is solely the author’s opinion and not investment advice – it is provided for educational purposes only. By using this, you agree that the information does not constitute any investment or financial instructions. Do conduct your own research and reach out to financial advisors before making any investment decisions.

The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, www.deltec.io.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, www.deltec.io.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.